Are you drowning in debt, unable to make ends meet? You’re not alone. Millions of Americans struggle with debt every year, but there is hope.

Debt consolidation is a viable solution that can help you manage your debt and get back on track.

In this article, we’ll explore the ins and outs of debt consolidation, including its benefits, drawbacks, and how to get started.

Is Debt Consolidation Right for You?

Before considering debt consolidation, it’s essential to assess your financial situation and determine whether it’s the right solution for you. Start by making a list of your debts, including the balance and interest rate of each, as well as the minimum monthly payment. This will help you visualize your debt and identify opportunities to consolidate. Additionally, consider your credit score, as a good credit score can qualify you for better interest rates and terms.

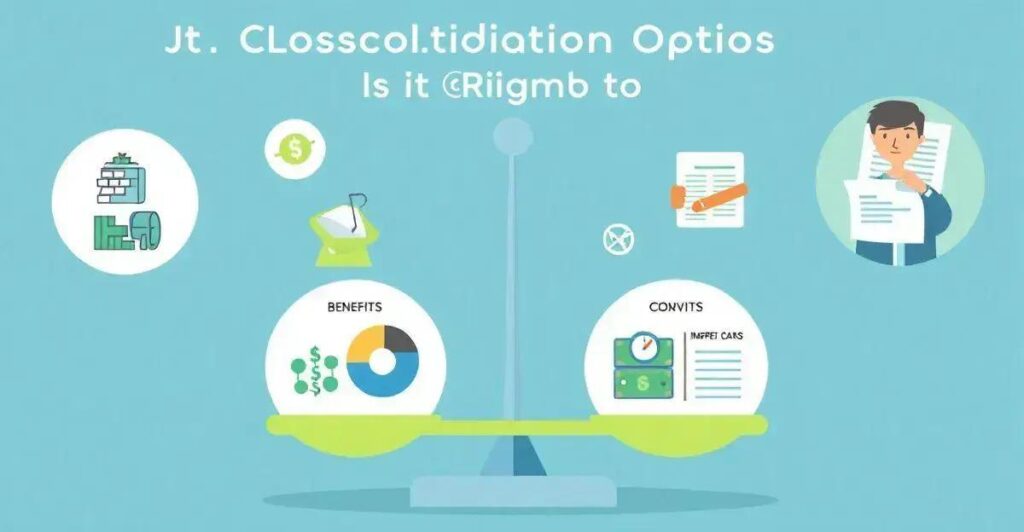

Debt consolidation offers numerous benefits, including reduced stress, lower interest rates, and a simplified payment process. By consolidating your debt, you can eliminate multiple payments and focus on a single, more manageable payment. This can also help you avoid late fees and penalties, which can save you money in the long run. Furthermore, debt consolidation can help you pay off your debt faster, as you’ll be applying a larger portion of your payment towards the principal balance.

To consolidate your debt, you’ll need to choose a debt consolidation method that suits your financial situation. Common methods include balance transfer credit cards, debt consolidation loans, and debt management plans. When selecting a debt consolidation option, consider the interest rate, fees, and repayment term to ensure you’re getting the best deal. Additionally, make sure you understand the terms and conditions of your chosen option, including any potential penalties for late payments.

There are several types of debt consolidation options available, each with its own advantages and disadvantages. For example, balance transfer credit cards can offer 0% interest rates for a promotional period, while debt consolidation loans can provide a lump sum payment to pay off multiple debts. Debt management plans, on the other hand, offer personalized guidance and support to help you manage your debt. When choosing a debt consolidation option, consider your financial goals, credit score, and debt amount to select the best fit for your situation.

While debt consolidation can be a powerful tool for managing debt, it’s not without its drawbacks. For example, debt consolidation loans can have higher interest rates than other options, and balance transfer credit cards may have fees for late payments. Additionally, debt consolidation may not be suitable for everyone, particularly those with high-interest debt or poor credit. It’s essential to carefully consider the pros and cons of debt consolidation before making a decision.

In conclusion, debt consolidation can be a valuable tool for managing debt and achieving financial stability. By understanding your financial situation, choosing the right debt consolidation option, and following a plan, you can pay off your debt and start building a stronger financial future. Remember to always prioritize your financial goals, stay disciplined, and avoid falling back into debt habits.

The Benefits of Debt Consolidation

Debt consolidation offers numerous benefits, including reduced stress, lower interest rates, and a simplified payment process. By consolidating your debt, you can eliminate multiple payments and focus on a single, more manageable payment. This can also help you avoid late fees and penalties, which can save you money in the long run. Furthermore, debt consolidation can help you pay off your debt faster, as you’ll be applying a larger portion of your payment towards the principal balance. By consolidating your debt, you can regain control of your finances and start building a stronger financial future.

When it comes to consolidating your debt, there are several methods to consider. One popular option is a debt consolidation loan, which provides a lump sum payment to pay off multiple debts. Another option is a balance transfer credit card, which can offer 0% interest rates for a promotional period. Additionally, debt management plans offer personalized guidance and support to help you manage your debt. It’s essential to carefully consider your financial goals, credit score, and debt amount to select the best debt consolidation option for your situation.

There are several types of debt consolidation options available, including debt consolidation loans, balance transfer credit cards, and debt management plans. Debt consolidation loans provide a lump sum payment to pay off multiple debts, while balance transfer credit cards offer 0% interest rates for a promotional period. Debt management plans offer personalized guidance and support to help you manage your debt. When choosing a debt consolidation option, consider your financial goals, credit score, and debt amount to select the best fit for your situation.

While debt consolidation can be a powerful tool for managing debt, it’s essential to be aware of the potential drawbacks. For example, debt consolidation loans can have higher interest rates than other options, and balance transfer credit cards may have fees for late payments. Additionally, debt consolidation may not be suitable for everyone, particularly those with high-interest debt or poor credit. It’s essential to carefully consider the pros and cons of debt consolidation before making a decision.

In conclusion, debt consolidation can be a valuable tool for managing debt and achieving financial stability. By understanding your financial situation, choosing the right debt consolidation option, and following a plan, you can pay off your debt and start building a stronger financial future. Remember to always prioritize your financial goals, stay disciplined, and avoid falling back into debt habits.

Debt consolidation is a viable solution for individuals struggling with debt, offering numerous benefits and options to help manage debt. By understanding the process, choosing the right option, and following a plan, you can regain control of your finances and start building a stronger financial future. Remember to stay disciplined, prioritize your financial goals, and avoid falling back into debt habits.

How to Consolidate Your Debt

To consolidate your debt, you’ll need to choose a debt consolidation method that suits your financial situation. Common methods include balance transfer credit cards, debt consolidation loans, and debt management plans.

When selecting a debt consolidation option, consider the interest rate, fees, and repayment term to ensure you’re getting the best deal. Additionally, make sure you understand the terms and conditions of your chosen option, including any potential penalties for late payments.

It’s also essential to create a budget and track your expenses to ensure you’re staying on track with your debt consolidation plan. By following these steps and staying committed, you can successfully consolidate your debt and start building a stronger financial future.

Types of Debt Consolidation Options

There are several types of debt consolidation options available, each with its own benefits and drawbacks.

Debt consolidation loans provide a lump sum payment to pay off multiple debts, while balance transfer credit cards offer 0% interest rates for a promotional period.

Debt management plans offer personalized guidance and support to help you manage your debt.

Additionally, debt settlement programs can help you negotiate with creditors to reduce the amount of debt you owe.

It’s essential to understand the pros and cons of each option and choose the one that best fits your financial situation and goals.

By considering your credit score, debt amount, and financial goals, you can select the most effective debt consolidation option and start working towards a debt-free future.

The Drawbacks of Debt Consolidation

While debt consolidation can be a valuable tool for managing debt, it’s essential to be aware of the potential drawbacks. One of the main drawbacks is the risk of higher interest rates and fees associated with debt consolidation loans.

Additionally, debt consolidation may not be suitable for everyone, particularly those with high-interest debt or poor credit. It’s also important to note that debt consolidation may not address the underlying causes of debt, such as overspending or poor budgeting habits.

Furthermore, debt consolidation can be a complex and time-consuming process, requiring careful planning and execution. Therefore, it’s crucial to carefully weigh the pros and cons of debt consolidation before making a decision.

Conclusion: Is Debt Consolidation the Answer to Your Financial Prayers?

In conclusion, debt consolidation can be a viable solution for those struggling with multiple debts. It allows individuals to combine their debts into a single payment, often with a lower interest rate, which can simplify their financial situation.

However, it is essential to consider whether this approach aligns with your financial goals. Debt consolidation is not a one-size-fits-all solution; it may work well for some but not for others.

Evaluating Your Options

Before deciding on debt consolidation, evaluate your current financial situation. Assess your total debt, interest rates, and monthly payments. Understanding your financial landscape will help you make an informed decision.

Additionally, consider the potential impact on your credit score and whether you can commit to the new payment plan. Staying disciplined and avoiding new debts during this process is crucial for success.

Ultimately, while debt consolidation can provide relief, it is essential to approach it with caution and a clear strategy. Seek advice from financial professionals if needed, and ensure that you are making the best choice for your financial future.

Frequently Asked Questions about Debt Consolidation

Is debt consolidation right for me?

Debt consolidation may be a good option for you if you’re struggling to manage multiple debts with high interest rates or fees. It can help simplify your payments and reduce your debt burden.

What are the benefits of debt consolidation?

Debt consolidation can help you pay off your debt faster, reduce your debt burden, and simplify your payments. It can also help you avoid late fees and penalties, and improve your credit score.

How do I consolidate my debt?

You can consolidate your debt by taking out a debt consolidation loan or credit card, or by working with a debt consolidation company. You can also try debt management plans or debt settlement programs.

What are the types of debt consolidation options available?

There are several types of debt consolidation options available, including debt consolidation loans, balance transfer credit cards, debt management plans, and debt settlement programs.

What are the drawbacks of debt consolidation?

Debt consolidation may not be suitable for everyone, particularly those with high-interest debt or poor credit. It can also be a complex and time-consuming process, and may require careful planning and execution.

Is debt consolidation the answer to my financial prayers?

Debt consolidation may be a helpful solution for managing your debt, but it’s important to carefully consider your financial situation and goals before making a decision. It’s also important to weigh the pros and cons of debt consolidation and choose the right option for your needs.